What is a Deed of Trust, and when is it needed?

Discover the purpose of a Deed of Trust in real estate, how it protects lenders, and when it is necessary.

Tired of nonsense pricing of DocuSign?

Start taking digital signatures with BoloSign and save money.

Introduction

In the world of real estate and property transactions, various legal documents play crucial roles in securing loans and protecting the interests of both lenders and borrowers. One such important document is the Deed of Trust. This comprehensive guide will explore the intricacies of a Deed of Trust, its purpose, how it differs from a mortgage, and why it's essential in certain real estate transactions.

What is a Deed of Trust?

It involves three parties: the borrower (trustor), the lender (beneficiary), and a neutral third party (trustee). The borrower transfers the legal title of the property to the trustee, who holds it as security for the loan provided by the lender.

The primary purpose of a Deed of Trust is to protect the lender's interests by ensuring they have a claim on the property if the borrower defaults on the loan. Unlike a traditional mortgage, which involves only two parties, a Deed of Trust introduces a third party - the trustee - who acts as an impartial intermediary between the borrower and the lender.

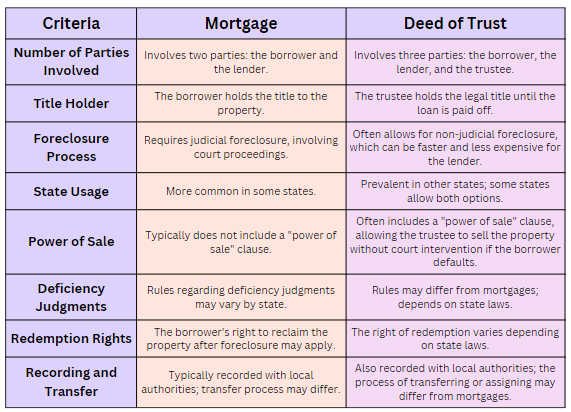

Deed of Trust vs. Mortgage

While both Deeds of Trust and mortgages serve similar purposes in securing real estate loans, there are several key differences between the two:

- Number of parties involved: A mortgage involves two parties - the borrower and the lender. A Deed of Trust involves three parties - the borrower, the lender, and the trustee.

- Title holder: In a mortgage, the borrower holds the title to the property. In a Deed of Trust, the trustee holds the legal title until the loan is paid off.

- Foreclosure process: Mortgages typically require judicial foreclosure, which involves court proceedings. Deeds of Trust often allow for non-judicial foreclosure, which can be faster and less expensive for the lender.

- State usage: Mortgages are more common in some states, while Deeds of Trust are prevalent in others. Some states allow both options.

- Power of sale: Deeds of Trust often include a "power of sale" clause, which allows the trustee to sell the property without court intervention if the borrower defaults.

- Deficiency judgments: In some states, the rules regarding deficiency judgments (when the sale price doesn't cover the outstanding loan balance) may differ between mortgages and Deeds of Trust.

- Redemption rights: The borrower's right to reclaim the property after foreclosure (known as the right of redemption) may vary between mortgages and Deeds of Trust, depending on state laws.

- Recording and transfer: While both mortgages and Deeds of Trust are typically recorded with local authorities, the process of transferring or assigning these documents to other lenders may differ.

To illustrate these differences, let's consider a hypothetical scenario:

Imagine two neighbors, Alice and Bob, purchasing homes of equal value in different states. Alice lives in a state that uses mortgages, while Bob's state primarily uses Deeds of Trust.

Alice's mortgage involves just her and her lender. If she defaults on her loan, the lender must go through the courts to foreclose on the property. This process can take several months or even years, depending on the court's backlog and any legal challenges Alice might raise.

Bob's Deed of Trust involves him, his lender, and a trustee. If Bob defaults on his loan, the trustee can initiate a non-judicial foreclosure process. This typically involves sending notices to Bob and publishing the foreclosure sale in local newspapers. The entire process can often be completed in a matter of weeks.

In Alice's case, she retains the title to her property throughout the loan term. The trustee holds the legal title for Bob, although he retains the right to use and enjoy the property as long as he's not in default.

This example illustrates how the choice between a mortgage and a Deed of Trust can significantly impact the rights and processes involved in a real estate transaction. Both borrowers and lenders must understand these differences when entering a real estate financing agreement.

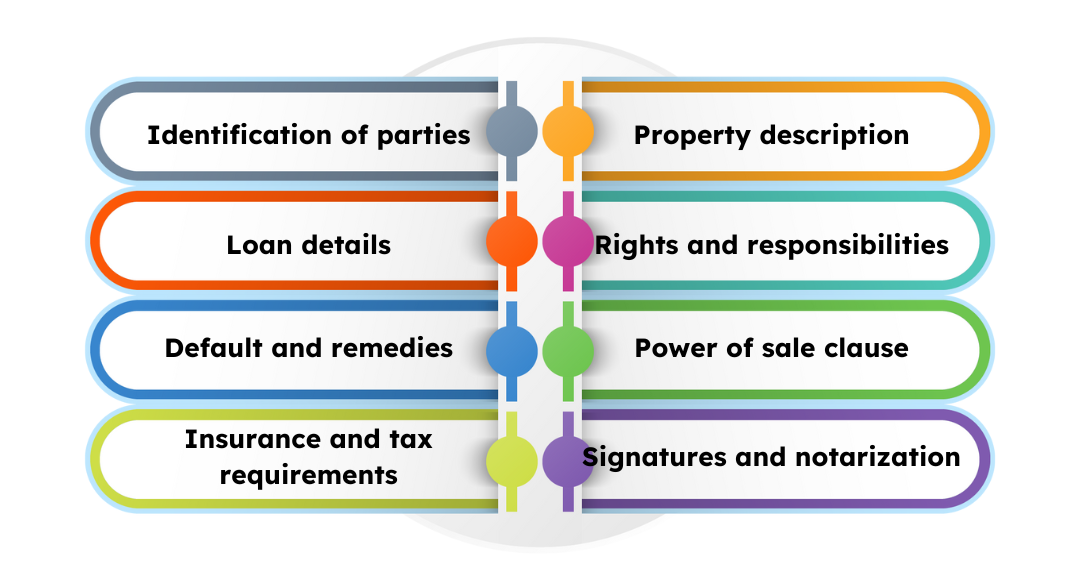

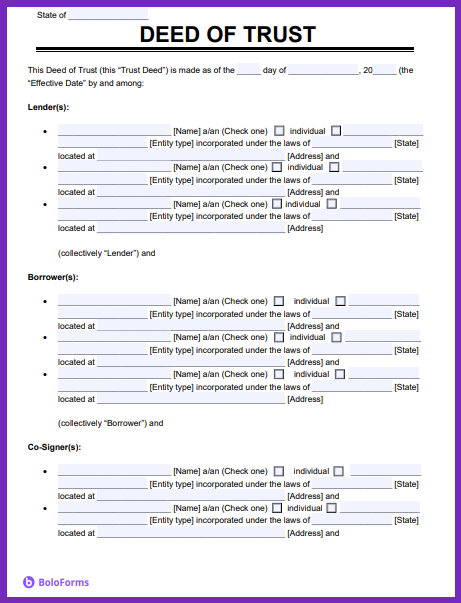

What Should I Include in a Deed of Trust?

A well-drafted Deed of Trust should include several key elements:

- Identification of parties: Clearly state the names and roles of the borrower, lender, and trustee.

- Property description: Provide a detailed legal description of the property being used as collateral.

- Loan details: Include the loan amount, interest rate, repayment terms, and duration.

- Rights and responsibilities: Outline the rights and obligations of each party involved.

- Default and remedies: Specify what constitutes a default and the actions that can be taken in such cases.

- Power of sale clause: Include this clause to allow non-judicial foreclosure if permitted by state law.

- Insurance and tax requirements: Specify the borrower's obligations regarding property insurance and property taxes.

- Signatures and notarization: Ensure all parties sign the document and have it notarized.

When Do I Need a Deed of Trust Form?

You may need a Deed of Trust form in the following situations:

- Real estate purchases: When buying a property using borrowed funds in states that use Deeds of Trust.

- Refinancing: When refinancing an existing mortgage in states that prefer Deeds of Trust.

- Private lending: When borrowing money from a private lender for real estate transactions.

- Seller financing: In cases where the property seller is providing financing to the buyer.

- Investment properties: When securing loans for investment or commercial properties.

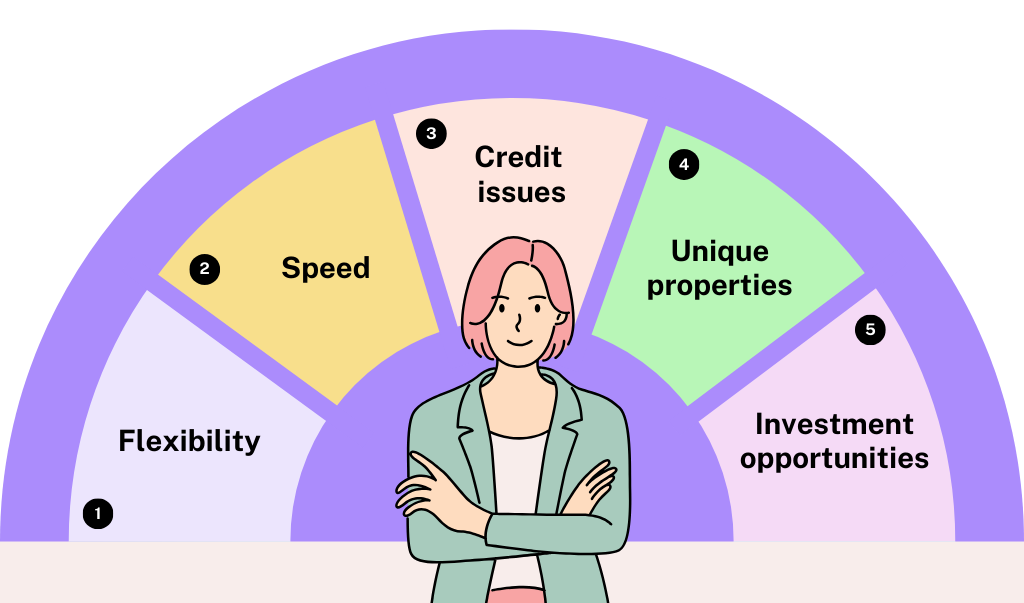

Why not just get a loan from the bank?

While traditional bank loans are common, there are several reasons why someone might opt for a loan secured by a Deed of Trust:

- Flexibility: Private lenders or alternative financing options may offer more flexible terms than traditional banks.

- Speed: The process of obtaining a loan through a Deed of Trust can sometimes be faster than going through a bank's lengthy approval process.

- Credit issues: Borrowers with less-than-perfect credit may find it easier to secure financing through private lenders using a Deed of Trust.

- Unique properties: Some properties may not qualify for traditional bank financing, making alternative options necessary.

- Investment opportunities: Real estate investors may prefer the speed and flexibility offered by private lenders and Deeds of Trust.

What Happens if I Don't Use a Deed of Trust Form?

Failing to use a Deed of Trust form when required can have several consequences:

- Lack of security: The lender may not have a secured interest in the property, making it difficult to recover their investment if the borrower defaults.

- Legal complications: Without a proper Deed of Trust, the terms of the loan and the rights of each party may be unclear, leading to potential legal disputes.

- Difficulty in enforcement: The lender may face challenges in enforcing their rights or initiating foreclosure proceedings if necessary.

- Higher risk for lenders: Without the security provided by a Deed of Trust, lenders may be less willing to offer loans or may charge higher interest rates to compensate for the increased risk.

- Potential regulatory issues: In some jurisdictions, failing to use the proper legal documents for real estate transactions may violate local regulations or lending laws.

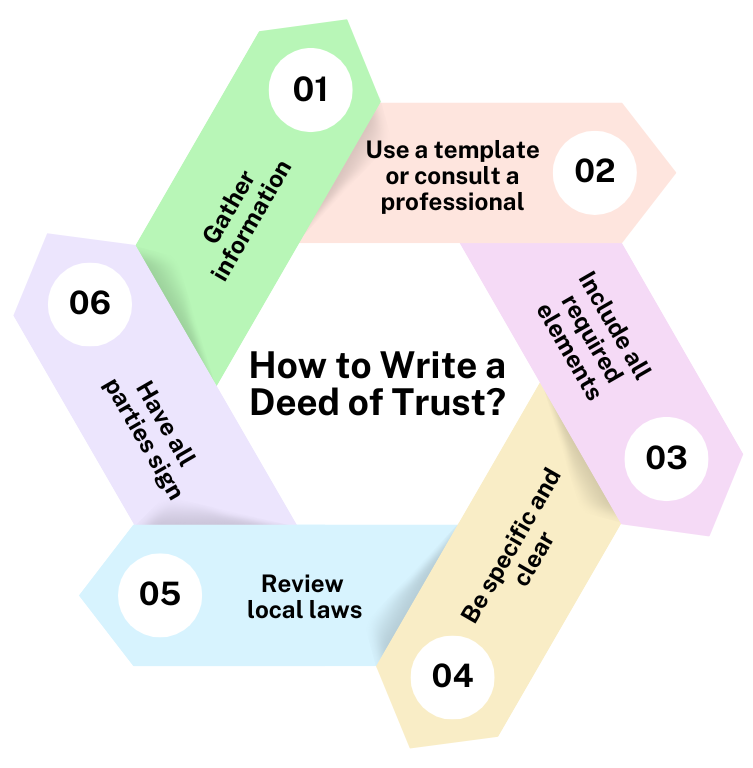

How to Write a Deed of Trust?

Writing a Deed of Trust requires careful attention to detail and knowledge of local laws. Here are the general steps to create a Deed of Trust:

- Gather information: Collect all necessary details about the parties involved, the property, and the loan terms.

- Use a template or consult a professional: Start with a state-specific template or seek assistance from a real estate attorney.

- Include all required elements: Ensure all essential components mentioned earlier are included in the document.

- Be specific and clear: Use precise language to avoid ambiguity and potential disputes.

- Review local laws: Ensure the document complies with state-specific requirements and regulations.

- Have all parties sign: Obtain signatures from the borrower, lender, and trustee.

What is the role of the trustee in a Deed of Trust?

The trustee plays a crucial role in a Deed of Trust arrangement:

- Holding title: The trustee holds the legal title to the property until the loan is paid off.

- Impartial intermediary: Acts as a neutral third party between the borrower and lender.

- Foreclosure proceedings: If the borrower defaults, the trustee is responsible for initiating and carrying out the foreclosure process.

- Reconveyance: Once the loan is paid off, the trustee transfers the legal title back to the borrower through a deed of reconveyance.

- Document management: The trustee may be responsible for holding and managing important documents related to the property and loan.

BoloSign: E-Signature Platform for Small Businesses

BoloSign is an innovative e-signature platform designed specifically for small businesses. It offers a comprehensive solution for signing and managing various documents, including Deeds of Trust. Here's why BoloSign is an excellent choice for handling your Deed of Trust and other legal documents:

- User-friendly interface: BoloSign provides an intuitive platform that makes it easy to create, send, and sign documents electronically.

- Legal compliance: The platform ensures that all e-signatures are legally binding and compliant with relevant regulations.

- Document templates: BoloSign offers a variety of templates, including ones for Deeds of Trust, making it easier to create professional documents quickly.

- Secure storage: All signed documents are securely stored in the cloud, allowing easy access and management.

- Collaboration features: Multiple parties can review and sign documents, making it ideal for Deed of Trust transactions involving borrowers, lenders, and trustees.

- Audit trails: BoloSign maintains detailed audit trails, providing a clear record of all document activities.

- Integration capabilities: The platform can integrate with other business tools, streamlining your document workflow.

How to Easily Manage Your Deed of Trust Contracts with BoloSign

BoloSign, an eSignature platform, provides a range of benefits for managing legal documents. It offers pre-made templates, including the Deed of Trust contract, which you can easily customize and send out for signatures, simplifying your document management process.

BoloSign offers a specialized Deed of Trust contract template that includes:

- Customizable fields for property details, borrower, lender, and trustee information.

- Automatic calculations for any relevant financial terms or loan details.

- E-signature fields for all parties involved, ensuring a quick and efficient signing process.

BoloSign offers a 7-day free trial, allowing you to experience its features and benefits firsthand. By trying BoloSign today, you can streamline your Deed of Trust process and other document signing needs, saving time and ensuring legal compliance.

Frequently Asked Questions

Can a Deed of Trust be used in all states?

No, not all states use Deeds of Trust. Some states exclusively use mortgages, while others allow both options.

How long does a Deed of Trust remain in effect?

A Deed of Trust typically remains in effect until the loan is fully repaid or the property is sold.

Can a Deed of Trust be transferred to another lender?

Yes, a Deed of Trust can be transferred or assigned to another lender, usually through a document called an "Assignment of Deed of Trust."

Is a Deed of Trust recorded publicly?

Yes, Deeds of Trust are typically recorded with the county recorder's office and become part of the public record.

Can a borrower sell a property with a Deed of Trust?

Yes, but the loan secured by the Deed of Trust usually needs to be paid off at the time of sale, or the new buyer must assume the existing loan.

Conclusion

A Deed of Trust is a vital legal instrument in real estate transactions, offering security for lenders and an alternative to traditional mortgages. Understanding its purpose, components, and how it differs from a mortgage is crucial for anyone involved in property transactions where Deeds of Trust are used. By leveraging modern tools like BoloSign, small businesses can efficiently manage the creation, signing, and storage of Deeds of Trust and other important documents. Whether you're a borrower, lender, or real estate professional, having a solid grasp of Deeds of Trust will help you navigate property transactions with confidence and clarity.ShareRewrite

Paresh Deshmukh

Co-Founder, BoloForms

7 Apr, 2025

Take a Look at Our Featured Articles

These articles will guide you on how to simplify office work, boost your efficiency, and concentrate on expanding your business.