Pros and Cons of a Partnership

Discover the advantages and challenges of partnerships. Make informed decisions for business collaboration. Explore insights now!

Tired of nonsense pricing of DocuSign?

Start taking digital signatures with BoloSign and save money.

Introduction

If you're contemplating teaming up with one or more business associates to pursue common goals, forming a partnership could be the right choice for you. Essentially, a business partnership is a legal arrangement in which two or more individuals collaborate to advance shared interests.

Each partner contributes their investment in various forms, which can include capital, property, labor, skills, contacts, or other assets, and they collectively share both the profits and losses of the business. Unlike certain other business structures, a partnership doesn't necessitate the creation of a legally distinct entity apart from the founding members. Selecting the appropriate business model is a crucial decision that can have a significant impact on your business's legal standing, structure, and day-to-day operations. Therefore, it's essential to make an informed choice that aligns with your specific circumstances.

Before you and your prospective partners put pen to paper and formalize your partnership agreement, it's vital to have a comprehensive understanding of the advantages and disadvantages of a partnership associated with this business structure.

What is a Partnership?

A partnership is a type of business structure in which two or more individuals or entities come together to jointly operate and manage a business. In a partnership, the partners share both the responsibilities and the profits and losses of the business. There are several forms of partnerships, but the most common ones include:

- General Partnership (GP): In a general partnership, all partners share equal responsibility for the management of the business and are personally liable for the business's debts and obligations. This means that the personal assets of the partners are at risk.

- Limited Partnership (LP): A limited partnership has both general partners and limited partners. General partners are actively involved in day-to-day operations and are personally liable for the business's debts. Limited partners, on the other hand, have limited liability and primarily invest capital into the business. Limited partners typically don't participate in the management of the business.

- Limited Liability Partnership (LLP): An LLP is a partnership structure that provides partners with limited liability, protecting their assets from the business's debts and liabilities. This structure is often used in professional service industries, such as law or accounting.

Partnerships can be an attractive option for small businesses, as they offer shared decision-making, shared profits, and flexibility in management. However, they also come with certain disadvantages, including the potential for personal liability (in the case of general partnerships) and the risk of conflicts among partners.

It's important to draft a comprehensive partnership agreement that outlines the roles, responsibilities, profit-sharing, and dispute-resolution mechanisms to ensure the smooth operation of the partnership and to protect the interests of all parties involved.

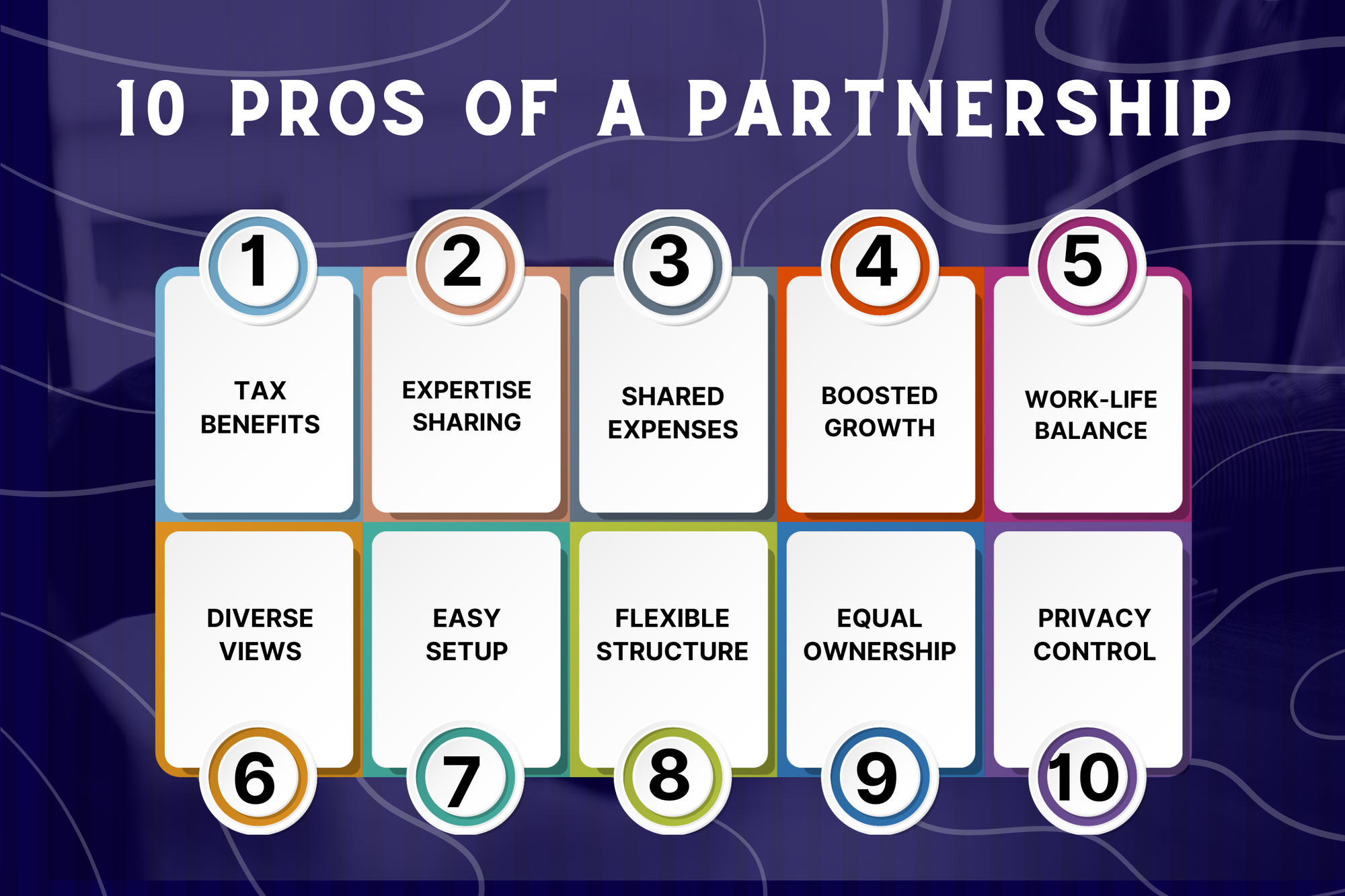

10 Pros of a Partnership

Creating a partnership offers distinctive benefits that can impact various facets of your business, encompassing financial aspects, tax considerations, work-life equilibrium, and overall productivity.

- Tax Benefits and Pass-Through Profits: Partnerships enjoy a unique tax advantage. Instead of paying income tax directly, they follow a "pass-through" model where profits and losses are distributed to the individual partners. Each partner then reports their share on their personal tax returns, potentially resulting in lower overall taxation for the business.

- Leveraging Complementary Expertise: Partnering brings together individuals with diverse skills and knowledge. These complementary skill sets can be a driving force behind a partnership's success. Partners often fill gaps in expertise, enhancing the overall capabilities of the business. For instance, one partner may excel in sales and business development, while the other is a certified accountant, creating a well-rounded team.

- Shared Overhead and Expenses: Overhead costs can be a significant challenge when starting a business. Partnerships alleviate this burden by allowing partners to share startup expenses and other operational costs. This collaborative approach is especially appealing for resource-intensive endeavors.

- Boosted Productivity and Growth: Partnerships facilitate a more manageable workload and shared responsibilities, which can lead to increased productivity. Moreover, partners can tap into each other's networks and connections, opening up unforeseen growth opportunities.

- Improved Work-Life Balance: Having a partner lightens the load and enables a healthier work-life balance. Research suggests that improved work-life balance can enhance productivity, making it a valuable aspect of a partnership. If a partner wishes to exit the partnership, an assignment of partnership interests can facilitate a seamless transition to a new partner.

- Diverse Perspectives: Partnerships thrive on diverse perspectives. Partners bring different viewpoints to the table, offering valuable insights and alternative viewpoints when crucial decisions need to be made.

- Reduced Formalities and Simplified Registration: Partnerships enjoy a streamlined process when it comes to registration. Most states recognize partnerships automatically once business operations begin. This simplicity contrasts with the more formal and bureaucratic requirements of limited liability companies (LLCs) and corporations.

- Flexibility to Convert Business Structure: Partnerships offer flexibility. If, at a later stage, you require more protection for your business, it's relatively straightforward to convert your partnership into an LLC. This conversion usually involves submitting official documents to the Secretary of State's Office.

- Equal Ownership and Autonomy: Unlike corporations where external shareholders or a board of directors may dictate decisions, partnerships grant equal ownership and control to the partners. Partners answer primarily to each other, leading to greater autonomy in business operations.

- Privacy and Confidentiality: Partnerships enjoy a degree of privacy and confidentiality. They aren't obligated to publicly disclose financial and organizational information, as corporations often do. Publicly traded companies must provide annual reports and financial data to shareholders and the public. Partnerships, in contrast, can maintain a higher level of privacy regarding their business affairs.

These advantages make partnerships an appealing option for entrepreneurs and businesses looking for flexibility, shared responsibilities, and financial benefits, all while retaining a sense of independence and privacy.

10 Cons of a Partnership

While partnerships offer several advantages, they also come with inherent drawbacks. These disadvantages of a partnership underscore the importance of carefully choosing a reliable partner.

- Unclear Division of Responsibilities: In some partnerships, the roles and responsibilities of each partner may be unclear or unbalanced. This lack of clarity can lead to friction and inefficiencies in decision-making and day-to-day operations.

- Limited Access to Capital: While partnerships can pool resources from multiple partners, they may still have limited access to external sources of capital, such as venture capital or public funding. This can constrain the business's ability to expand or invest in new opportunities.

- Potential for Personal Disputes to Affect Business: Personal issues and disputes among partners can spill over into business matters, disrupting operations and decision-making. This can be especially problematic in small, closely held partnerships where personal relationships are closely intertwined with the business.

- Increased Liability: One significant drawback of general partnerships is the shared liability among partners. Each partner has unlimited personal liability, which means that your personal assets and finances are at risk for any negative business dealings your partner enters into. For example, if your partner takes out a loan for the business, and the business cannot meet the loan payments, creditors can pursue legal action against both partners and seize their personal assets, including bank accounts, vehicles, and homes.

- Reduced Autonomy: Partnerships require joint decision-making, with partners sharing equal authority unless otherwise specified in the partnership agreement. This can lead to compromises and a potential loss of autonomy, as partners need to work together on all major decisions. The need for consensus can sometimes slow down the decision-making process.

- Potential for Partner-Partner Conflict: Disagreements and conflicts between partners can strain the partnership, particularly in partnerships with only two individuals where there's no tie-breaking mechanism in place. Addressing how disputes will be resolved in the partnership agreement is crucial to prevent such conflicts from becoming detrimental to the business.

- Exit Strategy Complications: Creating a clear exit strategy is essential in a partnership. Problems may arise when one partner wishes to sell their share of the business, and the other partner(s) do not want to buy or continue the partnership. This can lead to disputes over valuation and the future direction of the business.

- Decreased Stability: Partnerships, while offering flexibility, can be less stable than incorporated organizations. The business's continuity can be disrupted by life events such as partner illness, birth, death, or unexpected circumstances. These events can significantly impact the business's ongoing operations.

- Perceived Lack of Prestige: Some investors and collaborators may view partnerships as informal business structures and prefer the prestige associated with limited liability companies or corporations. While informality can have its advantages, it might deter potential investors and partners seeking a more structured and formal business arrangement.

- Shared Profits: Partnerships distribute profits by the terms of the partnership agreement, which means that profits are shared among partners. While having multiple partners can potentially generate more revenue, it also means that this revenue must be distributed among all partners, impacting individual earnings.

Why BoloForms Reigns Supreme Among Small Businesses?

BoloForms Signature is a powerful digital signature platform designed specifically for the needs of small businesses. It helps residential and commercial agents, brokers, escrow companies, property managers, REITs, homebuilders, and developers manage their contract workflows with ease.

Here's what BoloForms offers:

- Simplified Electronic Signatures: Sign documents however you prefer - draw, type, or upload your signature. BoloForms makes it easy.

- Effortless Document Editing: BoloForms includes a built-in editor, allowing you to complete forms and sign electronically within the same platform.

- Seamless Document Sharing: Send documents to anyone who needs to sign and request their signatures with just a few clicks.

These core features are the foundation of BoloForms, allowing you to efficiently sign and manage all your business forms, contracts, agreements, and other important documents. But BoloForms goes beyond the basics, offering additional features specifically designed to address the unique challenges faced by businesses.

One standout feature is the availability of pre-made templates, which not only save you valuable time but also provide essential legal protection. These contract templates have undergone thorough scrutiny by legal experts to ensure compliance and reliability. Furthermore, these templates can be effortlessly customized and personalized to suit your specific requirements. Once signed, these contracts are legally binding offering you the peace of mind and legal security you need in business transactions.

BoloForms offers a diverse range of business templates that cater to your specific needs, including:

- Limited Partnership Agreement

- Limited Liability Partnership Agreement

- 50/50 Partnership Agreement

- Real Estate Partnership Agreement

- Small Business Partnership Agreement

These templates are meticulously designed to simplify and expedite the document creation and signing process.

Powerful Features of BoloForms Signature

BoloForms goes beyond simple e-signatures to provide a comprehensive suite of features designed to streamline your business document workflows:

- Guided Signing: Ensure smooth sailing for signatories with BoloForms' guided signing feature. It helps them complete forms accurately while capturing their e-signatures.

- Remote & Mobile Signing: Gone are the days of chasing signatures! BoloForms allows signers to complete agreements electronically from anywhere, on any device.

- Legal Audit Log: Maintain complete transparency and compliance with BoloForms' legal audit log. It keeps a detailed digital record of all your signed documents and agreements.

- Document Tracking: BoloForms' document tracking feature keeps you on top of your entire contract workflow, facilitating the timely completion of agreements.

- Unmatched Security: BoloForms prioritizes the security of your information. Robust firewalls, secure data hosting, and encryption work together to safeguard your sensitive data.

With this powerful toolkit, BoloForms empowers you to manage your business documents efficiently and with peace of mind.

FAQs

What are the pros and cons of a partnership?

Partnerships offer shared decision-making and reduced administrative burdens. They foster collaboration and diverse skill sets among partners. However, partnerships entail shared liability, risking personal assets. Disagreements may arise among partners, hindering progress. Partnerships lack the formal structure of corporations, posing challenges for stability.

What are the pros and cons of general partnership?

General partnerships offer simplicity and shared decision-making, fostering collaboration and diverse perspectives among partners. They require minimal formalities compared to other business structures. However, partners in general partnerships face shared liability, where each partner is personally responsible for the business's debts and obligations. Disagreements among partners can arise, potentially hindering decision-making and progress. Despite these drawbacks, general partnerships remain popular for small businesses seeking flexibility and collaboration.

What are the advantages and disadvantages of a partnership?

Partnerships are simple to create, and partners are given a great deal of control. However, partnerships can be difficult to dissolve, and conflicts between partners do occur. There are many similarities between sole proprietorships and partnerships. Both have relatively low start-up costs.

What are business partnerships’ pros and cons?

Partnerships offer shared decision-making and resource pooling, fostering collaboration and flexibility. However, they involve shared liability, risking personal assets. Disagreements among partners can arise, hindering progress. Partnerships lack the legal protections of corporations, potentially impacting long-term stability. Despite challenges, partnerships remain popular for their agility and collaborative nature.

Conclusion

In the dynamic world of business, making the right choice of business structure is paramount to your success. Partnerships present a unique blend of advantages and disadvantages, and whether their benefits outweigh their drawbacks depends on your specific circumstances and goals.

Partnerships can offer unmatched flexibility and an array of potential advantages, such as shared profits, reduced formalities, and the ability to leverage diverse skills. They can provide room for creativity, innovation, and shared decision-making that suits the needs of many entrepreneurial endeavors. However, the disadvantages, including personal liability, potential conflicts, and reduced autonomy, underscore the critical importance of selecting trustworthy partners and crafting a comprehensive partnership agreement.

- Service Agreement: Outline the terms of services from one party to another with our service agreement template.

- Purchase Agreement: Utilize our complimentary Purchase Agreement template to document and formalize the sale of an item.

- Corporate Resolution: If you need to put major company decisions in writing then use a corporate resolution.

Paresh Deshmukh

Co-Founder, BoloForms

27 Oct, 2023

Take a Look at Our Featured Articles

These articles will guide you on how to simplify office work, boost your efficiency, and concentrate on expanding your business.