How to Transfer Business Ownership?

Explore seamless strategies for transferring business ownership. From sole proprietorships to corporations, ensure a smooth transition process.

Tired of nonsense pricing of DocuSign?

Start taking digital signatures with BoloSign and save money.

Introduction

Whether you're a business owner looking to pass on your venture to someone else or planning for the future, understanding how to transfer business ownership is crucial. This article explores the various methods of transferring business ownership and the steps involved, providing valuable insights based on your business's structure. From selling your business to gifting shares to a family member, you'll find the guidance you need to navigate this essential aspect of entrepreneurship.

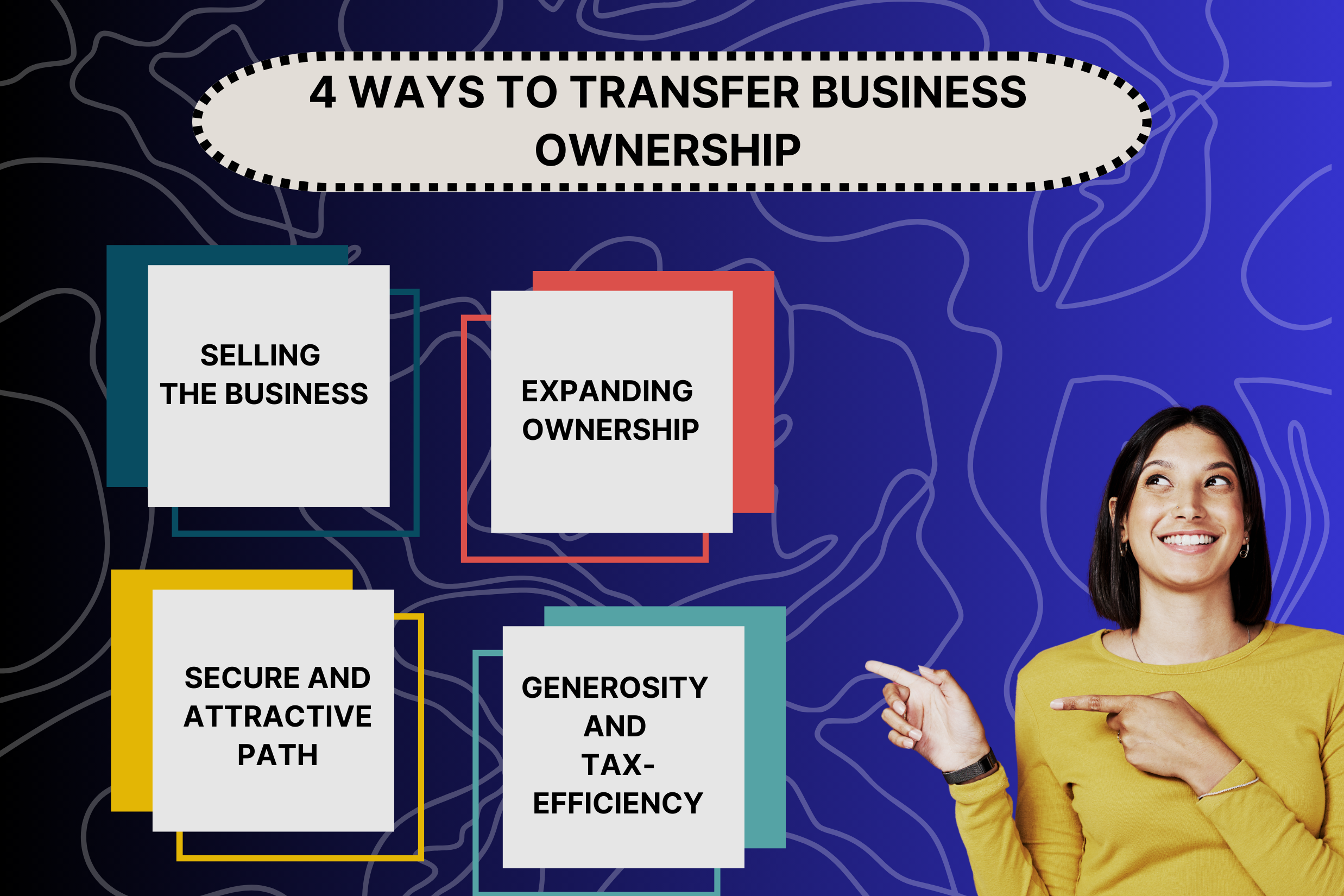

4 Ways To Transfer Business Ownership

Transferring business ownership can take different forms, each with its specific procedures and paperwork. Here are four common methods:

1. Selling the Business: A Common Transfer Method

One of the most prevalent methods for transferring business ownership is by selling the business. This can be accomplished through two primary approaches:

1. Cash Financing: In this scenario, both parties agree on a valuation for the business and its assets. The buyer then acquires your company by making an upfront payment in cash, which can come from their capital savings or through a loan.

2. Owner-Financing Sale: Alternatively, the buyer can opt for an owner-financing sale. Here, they purchase your company over a specified period, paying for it in installments.

Regardless of the chosen method, it's essential to establish a clear and legally binding framework to govern the transaction. To do this, you'll need to draft two critical documents:

A. Business Purchase Agreement: This comprehensive agreement outlines the terms and conditions of the sale, including the agreed-upon purchase price, asset valuation, and any specific conditions or warranties. It serves as the guiding document throughout the transfer process, ensuring both parties are on the same page.

B. Bill of Sale: The bill of sale is the official document used to transfer ownership from the seller to the buyer. It acts as tangible proof of the change in ownership, making it a crucial component in the transfer process.

2. Expanding Ownership or Reapportioning Shares: A Versatile Transfer Strategy

In scenarios where you own a partnership or a Limited Liability Company (LLC), transferring business ownership offers flexibility through two significant avenues:

1. Adding New Partners or Members: If you choose to add new partners or members to the business, these individuals will acquire ownership interests by investing in the company. As they purchase a majority of your share capital, they will subsequently assume the role of new owners of the company. This approach is particularly useful for those seeking to diversify ownership and potentially infuse new resources and expertise into the business.

2. Reapportioning Ownership: An alternative method for transferring ownership within your existing partnership or LLC is to reapportion the ownership structure. In this case, your current partners or members have the opportunity to buy shares from you, effectively redistributing the ownership within the organization. This approach can be beneficial when there's a desire to maintain the existing partnership or member base while altering the distribution of ownership shares.

3. A Secure and Attractive Path: The Lease-Purchase Method

For business owners seeking an approach to transfer ownership that appeals to a broad spectrum of potential buyers, the lease-purchase method offers an attractive and secure solution. This method leverages a lease-purchase agreement, which is advantageous for several reasons.

In a lease-purchase agreement, the lessee, initially a potential buyer, enters into a contract to lease the business over a specified duration. This arrangement provides numerous benefits to both parties involved in the transfer of business ownership:

- Attracting a Diverse Buyer Pool: The lease-purchase model has broad appeal, as it accommodates aspiring entrepreneurs, individuals interested in business ownership without substantial upfront costs, and those who wish to explore the venture before making a permanent commitment. This diversity in potential buyers increases the likelihood of successfully transferring ownership.

- Security and Flexibility for the Lessee: Lessees are attracted to this method because they pay for company ownership only during the lease period. This minimizes their financial risk, making it an accessible option for those who may not have the capital to purchase the business outright. Importantly, once the lease concludes, the lessee is empowered to make a critical decision. They can choose to renew the lease, solidify their ownership by purchasing the company, or, if their circumstances have changed, opt to terminate the relationship.

- Gradual Transition and Evaluation: The lease-purchase arrangement allows for a gradual transition of ownership, offering time for both parties to evaluate the fit and the performance of the business. This assessment period is invaluable for lessees who can thoroughly assess the company's operations, its market position, and its profitability before making a long-term commitment.

4. Generosity and Tax-Efficiency: Gifting or Bequeathing Business Ownership

Transferring business ownership through the act of gifting or bequeathing is a method underscored by both generosity and potential tax advantages. Whether you wish to pass your venture along to a family member or a close friend, this approach offers a seamless and cost-effective way to transition ownership.

Here's a closer look at gifting or bequeathing your business:

1. Bequeathing Ownership: Bequeathing involves transferring your business to a recipient through your last will. In this context, you specify your intentions for the business's future upon your passing. Notably, bequeathing company shares worth $16,000 or less annually can often be executed tax-free, a significant benefit for both the giver and the receiver. It provides an opportunity for a smooth and cost-efficient transition.

2. Gifting Ownership: Gifting, on the other hand, allows you to transfer business ownership during your lifetime. This can be particularly appealing if you wish to see the recipient take an active role in the company while you are still involved. Like bequeathing, gifting business ownership can also be structured to be tax-efficient, as there are tax exemptions and allowances that can apply.

Why Choose Gifting or Bequeathing?

The decision to gift or bequeath your business often stems from your desire to sustain the venture within your family or to see it continue in the hands of someone you trust. There are several compelling reasons to consider this approach:

- Generational Continuity: Gifting or bequeathing is an ideal method for maintaining your business within the family. It ensures the legacy and continuity of the company, passing it down through generations.

- Tax Efficiency: As previously mentioned, transferring business ownership through gifting or bequeathing can be accomplished with advantageous tax implications. Careful planning can allow you to minimize or even eliminate tax burdens.

- Smooth Transition: These methods facilitate a gradual transition, allowing the recipient to acclimate to their new role as a business owner. You can provide support, guidance, and mentorship during this transitional phase.

- Emotional Connection: Business owners often have strong emotional ties to their ventures. Transferring ownership through gifting or bequeathing ensures that the business remains in the hands of someone who understands and shares your passion for the company's mission and values.

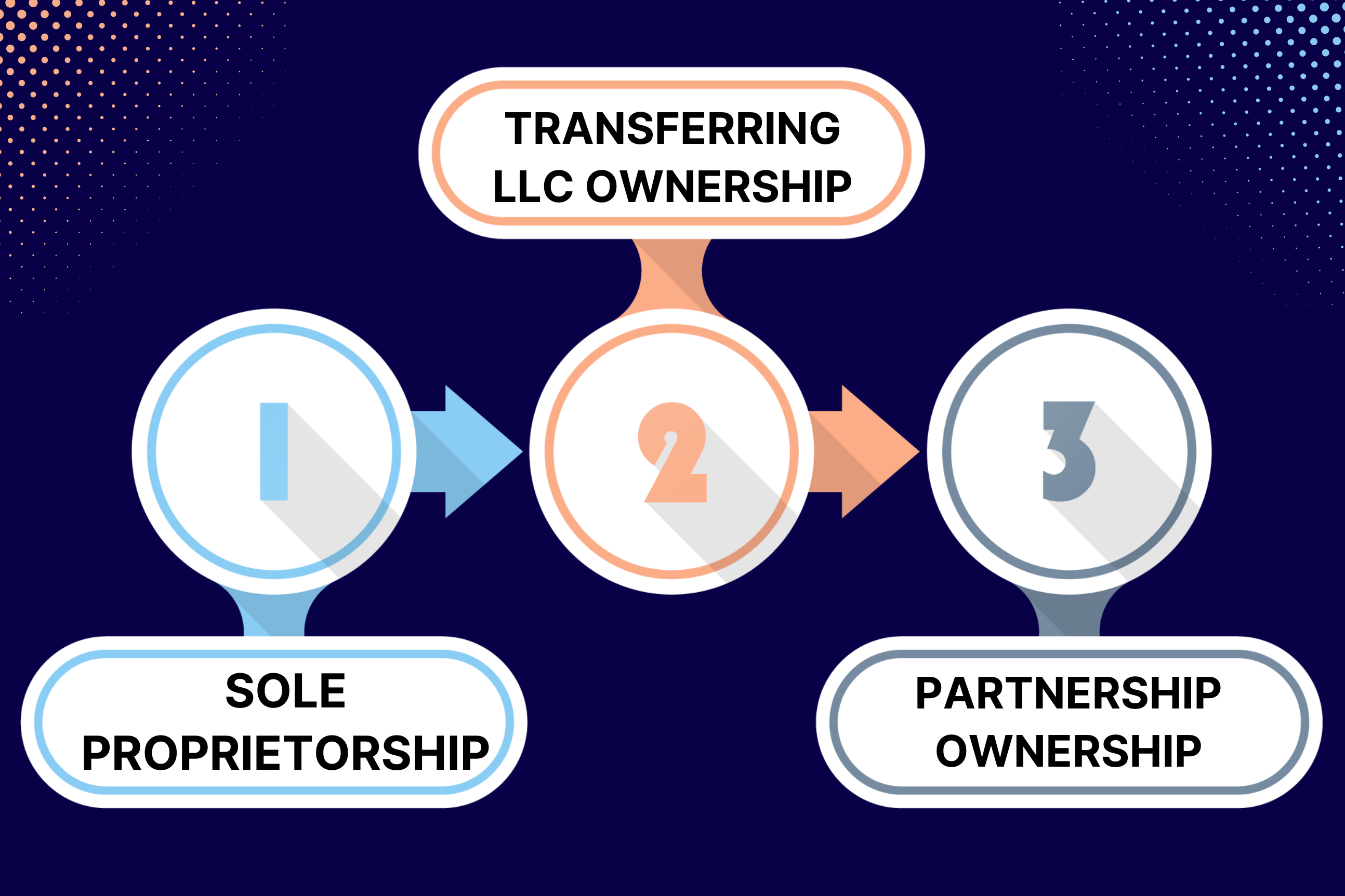

How to Transfer Business Ownership Based on Business Structure

Transferring LLC Ownership: A Strategic Approach

Transferring ownership of a Limited Liability Company (LLC) involves a series of carefully structured steps to ensure a seamless transition. Here's a comprehensive guide to navigating this intricate process:

1. Review Key Documents:

Articles of Organization and Operating Agreement: Commence by thoroughly reviewing your LLC's Articles of Organization and the Operating Agreement. These documents may contain specific guidelines and provisions related to selling the business.

2. Define the Buyer's Interests:

Engage with the Buyer: Initiate a dialogue with the prospective buyer to gain clarity on their specific objectives. Understanding whether they intend to acquire the entire LLC or select assets is vital. This step forms the foundation for subsequent negotiations.

3. Formalize Intent:

Letter of Intent (LOI): Declare your intention to sell the LLC by drafting a Letter of Intent (LOI). This document serves as an official notice of your commitment to the sale and outlines key terms and conditions.

4. Craft a Buy-Sell Agreement:

Outline Key Sale Details: Develop a comprehensive Buy-Sell Agreement that encapsulates all essential elements of the transaction:

- Timeline: Specify the timeframe within which the sale will transpire.

- Assets Included: Delineate the assets to be included in the sale.

- Nature of Transaction: Define whether the transaction pertains to specific assets or encompasses the entire LLC.

- Member Consent: Ensure the agreement secures the consent of all LLC members with ownership stakes.

- Additional Pertinent Details: Address any other relevant aspects of the sale.

- Notify Relevant Parties:

- Secretary of State: Following the sale's completion, promptly notify your Secretary of State regarding the change in ownership. Your lawyer can guide you through the specifics of this process.

- Additional Parties: Besides the Secretary of State, make it a priority to inform other pertinent parties, including the Internal Revenue Service (IRS), financial institutions where the LLC maintains accounts, your LLC's registered agent (the entity responsible for receiving official notices and documents), and states where your LLC is registered.

Sole Proprietorship Ownership Transfer

In a sole proprietorship, the business and its owner are inseparable. Consequently, you cannot sell the sole proprietorship itself. Instead, the process involves the sale or disposition of its assets.

For instance, if you run a thriving marketing firm as a sole proprietor and wish to retire, you can find a buyer for assets such as computers, customer lists, and the company name. Once you've assessed the value of these assets, and a buyer agrees to purchase them, you can proceed to draft and execute a sales contract. Upon the sale's completion, the sole proprietorship dissolves, and the buyer gains control of the acquired assets, utilizing them according to their discretion.

Transferring Ownership in a Partnership

Partnerships typically involve two or more owners, and if you find yourself in a position where you wish to transfer your ownership, you'll likely need to divest your share.

To successfully transfer ownership within a partnership, follow these steps:

- Review the Partnership Agreement: Begin by examining your partnership agreement, which outlines the ownership distribution among partners.

- Consult with Partners: Engage in discussions with your fellow partners to explore how your ownership shares can be reallocated. Document these arrangements within a buy-sell agreement.

- Transfer Interests: Act on the agreed-upon terms and transfer your ownership interests to the designated partners. Make sure to amend the partnership agreement to reflect these changes.

- Compliance with Jurisdiction: Depending on your jurisdiction's regulations, you might be required to file specific forms that declare the change in ownership.

Following this structured process ensures a smooth transition of ownership within your partnership, providing clarity and legal compliance throughout the transfer.

Role of Signatures in Business Ownership Transfer

Transferring ownership of a business is a significant undertaking, requiring careful planning and execution. One seemingly simple element plays a vital role in solidifying this process: signatures. Let's delve deeper into the importance of signatures in business ownership transfer and explore the different ways they function.

Authentication: Verifying Identity

In any legal document, a signature acts as a fingerprint, verifying the identity of the person signing. This ensures that the individuals claiming to be the seller (or sellers) and the buyer (or buyers) are indeed who they say they are. In the event of a dispute, a verified signature provides a crucial piece of evidence.

Intent: Demonstrating Agreement

By signing a business ownership transfer document, all parties involved are signifying their agreement to the terms and conditions outlined within. This includes details like the sale price, transfer of assets and liabilities, and any ongoing obligations. A signature makes it clear that everyone involved understands and accepts the terms of the transfer.

Record Keeping: Creating a Permanent Record

Signed documents serve as a permanent record of the business ownership transfer. Having a physical or digital copy with verified signatures protects all parties involved. Should any questions or disagreements arise in the future, the signed document becomes a crucial point of reference.

Types of Signatures in Business Ownership Transfer

Depending on the specific method of transfer and the legalities involved, different types of signatures may be required:

- Wet Signatures: The traditional method, involves signing a physical document with a pen. This is still a common practice and can be scanned for electronic records.

- Electronic Signatures (E-Signatures): With the rise of digital documents, e-signatures are becoming increasingly popular. These can be secured through various platforms that verify the signer's identity and create a tamper-proof record.

How Many Signatures Are Needed?

The number of signatures required will depend on the type of business entity and the transfer method. Here's a general breakdown:

- Sole Proprietorship: Typically, only the seller's signature is needed. However, if there are any loans or liabilities associated with the business, the lender or creditor may need to sign a release document.

- Partnership: All partners involved in the transfer will likely need to sign the agreement.

- Limited Liability Company (LLC): Members owning a majority of the ownership interests typically need to sign. Specific requirements may vary depending on the LLC's operating agreement.

- Corporation: Board members and authorized officers will likely sign on behalf of the corporation.

Boloforms as an E-Signature Platform

Boloforms Signature is an electronic signature platform that allows parties involved in a business transfer to sign agreements and documents online. This streamlines the process and creates a secure record. Perhaps Boloforms Signature offers pre-made templates for common business ownership transfer documents, such as purchase agreements or buy-sell agreements between partners. These templates could include designated signature areas.

Benefits of Utilizing Boloforms Signature

If Boloforms Signature offers the functionalities mentioned above, it could provide several benefits for business ownership transfer:

- Increased Efficiency: The online signing platform and pre-made templates could significantly expedite the transfer process.

- Enhanced Security: E-signatures and secure recordkeeping offered by Boloforms could bolster the overall security of the transaction.

- Streamlined Communication: A centralized platform for document storage and access could facilitate smoother communication and collaboration between the parties involved.

Considering a business ownership transfer? BoloForms Signature offers secure e-signatures and pre-made templates to make it easier.

Explore BoloForms now— https://www.boloforms.com/

FAQs

How do I transfer ownership of a business to a family member?

If you intend to transfer ownership of your business to a family member, a common approach is through gifting or bequeathing shares to them. Notably, this transfer can often be done without incurring taxes, provided you annually bequeath shares valued at $16,000 or less. By making this tax-efficient transfer, you can ensure a smooth transition of business ownership within your family.

How do I transfer ownership of a small family business?

Transferring ownership of a small family business varies by its structure:

- Sole Proprietorship: Sell assets for ownership transfer.

- Partnership: Transfer ownership interest among partners.

- Corporation: Transfer ownership via gifting, selling, or bequeathing shares.

- LLC: Review agreements, clarify buyer's intentions, draft buy-sell agreement, and notify relevant parties for a smooth transition.

Conclusion

Transferring business ownership is a significant decision for any entrepreneur. Whether you're selling your business, adding new partners, considering a lease-purchase agreement, or planning to gift your shares, understanding the process and the legal and financial implications is vital. By adhering to the specific procedures associated with your business structure, you can ensure a smooth transition and secure the future of your venture.

Signatures may seem like a formality, but they play a critical role in solidifying a business ownership transfer. By understanding their purpose and ensuring all parties involved sign the appropriate documents, you can ensure a smooth and legally sound transfer process. Remember, consulting an attorney is crucial to navigating the legalities and guaranteeing a successful ownership transition.

Paresh Deshmukh

Co-Founder, BoloForms

29 Oct, 2023

Take a Look at Our Featured Articles

These articles will guide you on how to simplify office work, boost your efficiency, and concentrate on expanding your business.